First published in Water e-Journal Vol 6 No 1 2021.

The list of countries that have committed to net-zero emissions by 2050 is growing. All Australian states and territories have committed to this target. It has prompted businesses in both the public and private sectors to begin developing and investing in strategies that contribute to a low carbon future.

The global climate policy instruments, particularly the Paris Agreement, provides the legal framework for countries to plan and deliver on their commitments to reduce their greenhouse gas (GHG) emissions. While the traditional energy sources (coal, gas, oil, solar and wind) will continue to play an important role in Australia’s future, the transition to a low carbon economy will require a diverse mix of other transformational low emission technologies.

Energy-from-waste technologies like direct combustion, gasification and anaerobic digestion will play a major role in the waste management sector to support state and national resource recovery goals including the transition to a circular economy. Renewable gas and hydrogen production, as well as carbon capture and storage will complement current efforts to decarbonise the industrial, transport, domestic and energy sectors.

This paper presents an overview of the policies relating to climate change and emissions reduction strategies in Australia, as well as a review of low emission technologies and investment opportunities for the water and waste sectors.

The COVID-19 pandemic is recognised as one of the major shocks of the 21st century. Nevertheless, there are important global ‘megatrends’ that are critical to the survival of humans and existing ecosystems. These megatrends are tied to economic recovery, representing challenges around growth and environmental sustainability. The global megatrends include climate change and resource stress, which stem from population growth, resource consumption and the need for more renewable technologies.

The Australian government has committed to reducing GHG emissions to 26 – 28% below 2005 levels by 2030. All Australian states and territories have an aspirational goal of achieving net-zero emissions by the mid-century. At a technical level, actions to reduce emissions might seem obvious. However, to be feasible, the economic and social implications of emissions reduction goals and proposed strategies are less well understood and need to be tested. Collaboration among government, businesses and the community is critical to developing a common understanding of pathways toward significant emissions reduction and sustainable, resilient economies simultaneously.

The objective of this paper is to explore the potential for low emission technologies in Australia by assessing the current policy context, identifying priority low emission technologies including investment opportunities, and presenting case studies relevant to the Australian water and waste sectors.

Over the last three decades, several global instruments have been developed to address climate change. The United Nations Framework Convention on Climate Change (UNFCC) in 1992 was a major milestone in the path towards addressing the climate change challenge globally. The adoption of the Kyoto Protocol in 1997 brought the UNFCC into operation. Through it, industrialised countries committed to limiting greenhouse gas (GHG) emissions by developing and adopting policies on mitigation and periodic reporting of emissions (UNFCC, 2008).

Following the 21st Conference of the Parties (COP21) in Paris in 2015, parties to the UNFCC reached a major agreement to accelerate actions needed for a sustainable low carbon future. COP21 resulted in the Paris Agreement being signed in 2016. It chartered a new direction in the global climate response and has been ratified by 186 countries to date. The central aim of the Paris Agreement is to keep the global temperature rise this century below two degrees Celsius, compared with pre-industrial levels.

In 2015, all United Nations Member States adopted the 2030 Agenda for Sustainable Development. At its core are 17 Sustainable Development Goals (SDGs) to address global challenges including poverty, inequality, climate change, environmental degradation, peace, and justice. Goal 13 specifically focuses on taking urgent action to combat climate change and its impacts.

The 2019 Climate Action Summit identified key sectors in which actions to combat climate change can make significant differences. These sectors include heavy industry, cities, nature-based solutions, energy, resilience, and climate finance. In the past two decades, the Global Climate Policy Framework has been instrumental in spearheading economic activities that put emphasis on emissions reduction and sustainability.

The Australian Government Department of Industry, Science, Energy and Resources is charged with leading the management and delivery of policies and programs relating to climate change strategies in Australia. These strategies are aimed at outlining domestic actions to reduce Australia’s emissions and meeting international climate change commitments. Other industry initiatives are continually being developed to complement government strategies.

The Technology Investment Roadmap will be a key element of Australia’s Long-term Emissions Reduction Strategy that Australia will take to the 26th UNFCCC climate summit in Glasgow scheduled in November 2021. The Roadmap will provide a framework to accelerate the development and commercialisation of low emission technologies (Department of Industry, Science, Energy and Resources, 2020).

A key milestone of the Roadmap was the development of the First Emissions Technology Statement in 2020. It highlighted the priority technologies and stretch goals, including the anticipated impacts of these, and the importance of public-private partnerships. The First Emissions Technology Statement identified clean hydrogen, energy storage, low carbon materials, carbon capture and storage (CCS) and soil carbon as the priority low emission technologies that have potential to substantially reduce emissions both in Australia and internationally across multiple sectors. These technologies will be the focus of new investments and the government will aim to remove barriers to commercialisation of these technologies.

The Council of Australian Governments (COAG) Energy Council released the National Hydrogen Strategy in 2019. The Strategy sets a pathway to develop Australia’s hydrogen industry and prioritise actions that accelerate commercialisation of hydrogen. The Strategy is centred around implementing an adaptive approach to take advantage of growth in domestic and global hydrogen demand.

The potential for Australia to become a major hydrogen exporter is realistic. Three of Australia’s top trading partners, Japan, South Korea, and China have made clear commitments to include hydrogen production and consumption in their decarbonisation strategies. The predicted increase in the penetration of renewable energy into the electricity supply mix in Australia, coupled with the foreseeable fall in the cost of fuel cells, will likely result in clean hydrogen being increasingly cost competitive. Hence Australia has a potential competitive advantage in developing an export industry for hydrogen.

In 2020, the Waste Management and Resource Recovery Association of Australia (WMRR) published its Energy from Waste (EfW) Roadmap to 2025. The Roadmap is designed to help overcome the key hurdles to developing EfW in Australia and outlines steps required to achieve the following six outcomes:

The successful implementation of the Roadmap will result in generation of renewable energy from waste that would otherwise go to landfill. Investment in the EfW sector will also stimulate the economy through creation of jobs and employment during the design, construction, and operation of these facilities.

Australia developed the Emissions Reduction Fund (ERF) and the Safeguard Mechanism as key instruments that provide a platform to incentives for emission reduction by Australian businesses. The ERF is a voluntary scheme that targets a variety of businesses and individuals, encouraging them to innovate, plan and implement applications and technologies to reduce their GHG emissions (Clean Energy Regulator, 2016). Under the ERF scheme, participants can earn Australian Carbon Credit Units (ACCUs) issued by the Clean Energy Regulator for activities undertaken as ‘eligible offset projects’ that result in emissions reduction. Each tonne of carbon dioxide equivalent (tCO2-e) avoided or stored by an eligible activity earns one ACCU. ACCUs can be sold either to the government or on a secondary market, subject to applicable carbon abatement contracts.

The Safeguard Mechanism supports the ERF in ensuring that eligible activities are not creating a rise in emissions elsewhere in the economy. The Safeguard Mechanism thus requires Australia’s largest GHG contributors to keep their net emissions below an emissions baseline.

Gas Vision 2050 was launched in 2017 by Energy Networks Australia and its industry partners. The vision described how gas and renewables can support each other in various domestic and industrial sectors along a path towards decarbonisation. The focus for most organisations has been to reduce emissions from electricity use. However, decarbonisation of gas has also gained attention and could present multiple opportunities. The key transformational technologies identified include biogas (and biomethane) production, hydrogen, and CCS. Central to this vision is the value of gas and gas infrastructure, particularly the potential cost-competitiveness of commercialising transformational technologies to using existing gas infrastructure rather than electrification (Energy Networks Australia, 2020).

The Australian Renewable Energy Agency (ARENA) is currently developing a Bioenergy Roadmap to provide a framework for how bioenergy can contribute to Australia’s energy transition and help reduce GHG emissions. The Bioenergy Roadmap will inform on investment opportunities and policy decisions in the Australian bioenergy sector.

Bioenergy is a renewable energy source produced from biomass or bioenergy feedstocks (Bauen et al., 2009). It provides a low emissions option for replacement or supplementing fossil fuels by providing cleaner alternatives in electricity, heat and transport applications. Bioenergy feedstocks typically include domestic and industrial waste, agricultural crops/residues, animal and plant waste, algae, and sewage sludge. These feedstocks can be converted into bioenergy using a wide range of technologies and processes. The more commonly used conversion technologies are conventional direct combustion, co-firing, gasification, pyrolysis, and anaerobic digestion. In Australia, bioenergy makes up less than 5% of the total energy consumption. In comparison, bioenergy in the European Union (EU) contributes over 10% of total energy consumption (KPMG, 2018). This presents numerous opportunities for Australia.

Low emission technologies improve emissions reduction from existing energy sources and facilitate development of low emission energy sources. The key technologies discussed in this paper include energy from waste, hydrogen production and carbon capture and storage.

Energy from waste (EfW) is the term used to describe the treatment of waste to harness energy from material that would otherwise go to landfill. The energy is created either by treating residual waste (i.e., waste that cannot be recycled) using high temperature treatment technologies (e.g., combustion or gasification) or by treating organic waste including sewage sludge, using biological anaerobic digestion for energy.

Anaerobic digestion

Anaerobic digestion (AD) is a traditional process that involves the breakdown of organic matter in an oxygen-free environment to generate a biogas and a digestate (Fagerström et al., 2018). Biogas typically consists mainly of methane (60% by volume) and carbon dioxide (40% by volume). The most common use of biogas is through internal combustion engines, converting biogas to electricity. Waste heat from the engine’s cooling system can be recovered and used for digester heating. This system of capturing electricity and heat simultaneously is referred to as co-generation or combined heat and power (CHP). Biogas can also be used in dedicated boilers for heat-only production. The adoption of AD technology has grown significantly in Australia and around the world over the last few decades, pursuant to energy and climate change drivers (McCabe et al., 2020). GHG emission reduction benefits associated with biogas production from organic waste residues can be realised from the following:

Direct combustion

Direct combustion, or conventional EfW, also commonly referred to as incineration, is a thermal treatment technology. It involves the complete combustion of carbon-based materials to generate electricity and/or heat (Tarukado et al., 2019). Conventional EfW is appropriate for wastes that are hazardous, non-biodegradable or wastes that cannot otherwise be re-used or recycled.

Direct combustion is a commercially mature technology that has been widely used, particularly in Europe, to treat residual waste from the municipal and industrial sectors and sewage sludge. The energy from direct combustion plants is typically recovered by CHP plants using the Rankine cycle for production of electricity and heat. Heat would typically be generated in the form of low-pressure, medium-pressure or high-pressure steam and can be used by nearby industrial users. Electricity generated can be used behind-the-meter or exported to the grid, reducing reliance on fossil-based electricity. In Australia, conventional EfW has a chequered history, often attributed to community concerns regarding public health risks from air emissions and climactic factors (for example, lower demand for waste heat in a hot climate).

Gasification

Gasification is a thermal treatment process that involves partial thermal oxidation of carbon-based materials (under sub-stoichiometric oxygen environments). The primary products are synthesis gas (commonly referred to as syngas) and a solid ash or char. Syngas containing primarily hydrogen, carbon monoxide and some carbon dioxide, is a precursor to a variety of chemicals, including synthetic natural gas, ammonia, and methanol. Syngas is also an energy carrier and can be directly combusted in the gasification energy recovery plant to generate electricity and/or heat. There is ongoing research investigating the agronomic benefits of the ash or char product for use as a soil amendment. Gasification requires pre-treatment of the incoming feedstock to ensure appropriate particle size and homogenisation of the waste stream. Gasification can also be used for the treatment of sewage sludge or biosolids. The flexibility of gasification in providing pathways for other high-value products makes this technology worth investigating. As an alternative to steam-methane reforming, coal gasification contributes significantly to global hydrogen production. As a result, gasification could play a major role in a potential future low-carbon Australian economy.

Hydrogen is a flexible, storable, and transportable fuel that can be produced through a variety of pathways using different feedstocks. Steam-methane reforming, coal or biomass gasification and electrolysis are among the common methods of generating hydrogen (Energy Networks Australia, 2019). When hydrogen is used as a fuel for energy, the only by-product is water resulting in no carbon emissions. This makes hydrogen a clean fuel. However, it is noted that the entire hydrogen production and utilisation value chain will most likely carry with it indirect GHG emissions, to some extent. For example, if fossil fuels are used to generate steam for hydrogen production via steam-methane reforming, the associated GHG emissions will need to be captured and stored or offset.

Hydrogen is a versatile fuel or feedstock that has many applications. Hydrogen can be used as a fuel, like natural gas for heating and cooking. Blending of hydrogen and natural gas using existing gas networks could be viable in the future. Hydrogen, through fuel cells can be used to produce electricity or power cars (IEA, 2019). It can also store surplus renewable energy when produced from electrolysis using solar or wind-generated power. This presents opportunities for Australia to export its renewable energy resources to other countries.

While hydrogen offers benefits and opportunities, producing hydrogen particularly from electrolysis also requires water. This could present constraints in drought-impacted parts of Australia. Ideal production sites would need to have access to renewable energy and sustainable water supplies. Opportunities exist in the water sector to develop recycled water schemes that would supply water at these hydrogen production sites. However, high purity water is required for electrolysis and this poses additional challenges around treatment, energy requirements, and disposal of waste streams.

Carbon capture and storage involve processes that capture and safely inject large quantities of carbon dioxide deep underground, instead of letting the gas escape to the atmosphere. The common technologies include pre and post-combustion capture and oxy-fuel combustion systems (Freund & Kaarstad, 2007). CCS will most likely play a crucial role in combatting climate change. Decarbonisation pathways include a diverse mix of strategies. These strategies rely on a high level of commitment from multiple stakeholders, and the extent to which radical changes in both technology and human behaviours can be achieved. Given the central role that oil and gas, cement, iron and steel industries play in the economies of many countries (including Australia), achieving significant emissions reduction in these hard-to-abate industries will be challenging. CCS could provide cost-effective solutions in the medium-long term, especially if the goal of achieving net-zero emissions by 2050 is to be pursued and realised.

CCS can complement renewable energy in pathways to reduce emissions. For example, while green hydrogen can be produced by the electrolysis of water using renewable solar and wind energy, there are regions whereby coal and natural gas will continue to provide low-cost energy and electricity. In these regions, hydrogen production from coal or natural gas, coupled with CCS, will likely be a low-cost option to help decarbonise hard-to-abate industries.

The National Waste Policy Action Plan sets a target of 80% average resource recovery rate from all waste streams by 2030 (Department of the Environment, 2019). The national resource recovery rate in 2018-19 was 63% (Blue Environment, 2020). To achieve the 2030 national resource recovery target, a fully integrated waste and resource recovery system, which includes energy from waste, will be critical. Hence EfW facilities that turn urban waste into energy are a major investment opportunity in Australia.

Anaerobic digestion facilities

With national and state targets to reduce the amount of organic waste disposed to landfill, anaerobic digestion can provide opportunities to manage this waste stream and generate sustainable energy. AD facilities will likely be a viable waste management option for local urban and regional councils collecting source separated organic waste particularly from the domestic and commercial and industrial sectors. For example, Yarra Valley Water developed a stand-alone AD plant next to their Aurora sewage treatment plant in 2017. The AD plant processes approximately 33,000 tonnes of commercial food waste per year, generating around 22,000 kilowatt-hours of electricity per day, enough to power the equivalent of around 1300 homes.

In 2015, Biogas Renewables commissioned the Jandakot Bioenergy Plant in Perth. The plant uses AD technology to process between 35,000 – 50,000 tonnes per year of food waste sourced from the commercial and industrial sector. The facility can generate around two megawatts of baseline electricity and can export 1.7 megawatts to the local electricity grid.

In New Zealand, construction of the nation’s first large-scale food waste-to-bioenergy plant is underway at Reporoa, located in central North Island. The facility will be operational in 2022 and will process around 75,000 tonnes of organic waste from businesses and household food waste collection facilities on North Island. The energy generated will be enough to power the equivalent of 2500 homes. Furthermore, the undigested material will be processed into a clean bio-fertiliser for use at a local farmland. Heat and carbon dioxide will be harnessed and used at a local greenhouse, thus maximising resource recovery.

Commercial deployment of AD plants is anticipated to increase in the medium to long term, if federal and state governments continue to develop policy frameworks and regulatory environments that support adoption of AD. This will present economic development and investment opportunities.

Thermal EfW facilities

While AD technology can be adopted for the management and treatment of the organic fraction of domestic, commercial, and industrial waste streams, there would still be a residual waste fraction destined for landfill disposal. Particularly for those residual wastes, thermal EfW technologies can play a part. Australian states and territories have different policies or position statements on EfW. There is no nationally consistent policy framework that outlines Best Practice principles and requirements for these facilities. This lack of a national standard approach to EfW has created significant hurdles and slowed down development of the EfW sector in Australia.

While there are significant barriers to the widespread adoption of thermal EfW across Australia, there have been some successes in the past few years including major projects reaching financial close and some currently under construction. The Avertas Energy project will be Australia’s first thermal EfW plant. The project is located in the Kwinana Industrial Area, located approximately 40km south of Perth. Macquarie Capital and the Dutch Infrastructure Fund (DIF) are leading the development of this project, with a total capital investment of approximately $700 million (DIF Capital Partners, undated). The EfW plant will process approximately 400,000 tonnes per year of residual domestic, commercial, industrial and construction and demolition waste to generate around 36 megawatts of baseload power for export to the grid. The emissions reduction estimated for this project will be the equivalent of taking 85,000 cars off the road.

Another project in the Rockingham Industrial Zone was approved in Western Australia and is currently under construction. This EfW plant will have a total capital investment of around $515 million and will process around 300,000 tonnes of municipal, commercial, and industrial waste per year to generate approximately 29 megawatts of power. The EfW facility will be jointly owned by a consortium of investors, including Hitachi Zosen Inova (HZI), ACCIONA and John Laing. SUEZ will operate and maintain the facility and supply 65,000 tonnes of commercial and industrial waste per year.

With numerous EfW projects in the planning phase in other states, each represents a significant milestone in the pathway towards commercialisation of thermal EfW in Australia, reflecting significant investment opportunities in this sector.

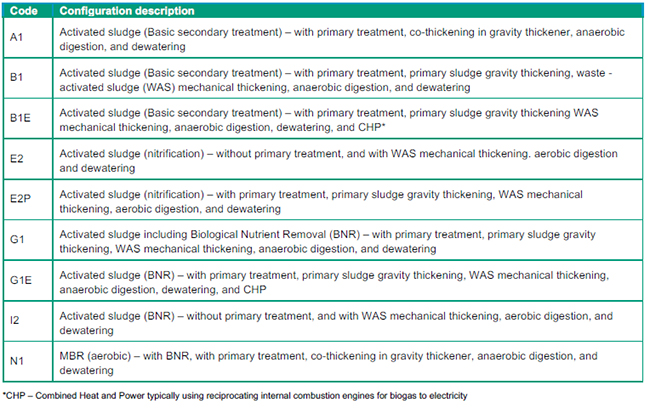

The water industry is currently facing numerous challenges, risks and opportunities to which utilities must respond. Some of the key challenges include the pressures of ageing infrastructure and a growing population, changing planning and regulatory environments, transitioning energy markets, technology changes and climate change impacts. These challenges are linked to the global megatrends and tend to drive major changes in asset management, requiring substantial investment in water and wastewater treatment infrastructure. Investment opportunities from infrastructure upgrades or improvements, to service growth for water and wastewater treatment systems, depend heavily on the configuration of existing process unit operations. There are various best-practice facility configurations used for domestic wastewater treatment in the developed world, some of which are summarised in Table 1 below:

For many water utilities, capital works for wastewater treatment infrastructure upgrades that could have a significant impact on the treatment plant’s overall energy balance would typically include modifications to the incoming solids capture process, primary followed by secondary treatment, nutrient removal, and sludge stabilisation processes. As noted in Table 1, there are some facility configurations without primary treatment, anaerobic digestion, and CHP. These can be viewed as missed opportunities that can be exploited, where technically feasible and financially viable, to significantly reduce lifecycle energy requirements, operational costs as well as GHG emissions. Some of these strategies are described in the following sections.

Adopting anaerobic digestion and co-generation

Adopting AD combined with CHP at WWTPs (existing and new) can turn these facilities into water resource recovery facilities (WRRFs) presenting unique opportunities to a circular economy for the water industry.

In Australia, AD technology has predominantly been applied to reduce the environmental footprint of industrial wastewaters, particularly dairy and piggery effluents. Unfortunately, the uptake rate of AD technology for bioenergy generation at WWTPs in Australia is still much lower than in Europe and North America. This can be attributed to the lack of strong policy drivers and bioenergy generation incentives in Australia on one hand, and on the other, a strong drive towards BNR technology with low effluent nutrient environmental consents, particularly along the east coast. BNR activated sludge process design tended in the past to move away from primary treatment with AD. Increased use of chemicals to supplement nutrient removal is one alternative, making AD and BNR compatible, but this increases complexity and cost.

It is noted that electricity costs and sludge transport/disposal costs can account for more than 50% of total operational costs in most wastewater treatment plants, while also contributing significantly to the overall carbon footprint. Furthermore, onsite generation and use of bioenergy at WWTPs reduces exposure to large energy price volatility and provides a more reliable energy supply. This presents investment opportunities to upgrade underutilised AD infrastructure to effectively capture and generate bioenergy or to develop new and dedicated AD facilities that could be co-located with other organic waste generators.

Implementing co-digestion

Co-digestion is a process whereby energy-rich organic waste from domestic, commercial, and industrial sectors (such as food waste, beverage waste, etc.) are added to digesters treating wastewater sludge. For utilities that currently operate AD plants at existing WWTPs, there might be opportunities to utilise spare digester capacity through implementation of co-digestion. This process has demonstrated several benefits:

Sydney Water has been using co-digestion to convert organic waste and sewage sludge into renewable energy at Bondi WWTP (Australian Water Association, 2016). Results from the trials demonstrated energy-self-sufficiency could be achieved including production of surplus energy, noting that Bondi WWTP does not have full treatment to secondary effluent (i.e., lower site energy use compared to more advanced WWTPs). Co-digestion can also be a viable option for greenfield developments that seek to leverage integrated land use opportunities through co-location of infrastructure and co-processing of waste streams.

Biogas upgrading to biomethane

Over the medium term, large-scale grid-sourced wind and solar might become a lower cost option than onsite co-generation for many biogas plant operators. By contrast, market dynamics including energy and climate change drivers will likely increase the cost of transport fuels and natural gas over this timeframe. As a result, high-value markets for biogas would need to be explored and investigated. Biomethane could provide significant investment opportunities. This renewable gas has been identified as a key decarbonisation pathway in Gas Vision 2050 (Energy Networks Australia, 2020).

Biomethane is a renewable form of natural gas made from biogas. Biomethane generally has a methane concentration of 96-98% by volume. Due to the high methane concentration, biomethane has a higher energy density and burns ‘cleaner’ than biogas. It can be produced either by refining biogas, via removal of carbon dioxide and other contaminants using upgrading technologies, or through biomass gasification followed by methanation. The latter technology is not commonly used.

Biomethane can be conditioned and utilised as biomethane liquified natural gas (BioLNG) or can be compressed for use as biomethane compressed natural gas (BioCNG). As a result, upgrading biogas to biomethane for use as a transport fuel or for export to the natural gas network will open new and higher value markets and opportunities for businesses while significantly decarbonising the Australian transport and gas sectors.

Currently, biomethane production in Australia does not appear to be financially viable. However, Sydney Water, in a joint initiative with Australian Renewable Energy Agency (ARENA) and Jemena, will develop a demonstration scale facility. This plant will upgrade biogas produced from the anaerobic digestion of sewage sludge at Sydney Water’s Malabar WWTP (ARENA, 2020). The biomethane generated will be injected into Jemena’s gas distribution network. It is anticipated that once operational in 2022, the $14 million dollar project will provide operational data and experience to inform future upscaling and investment decisions. This technology has been demonstrated to be economically viable particularly in Europe and North America and will likely be a priority area in developing Australia’s bioeconomy.

Biosolids gasification

Many water utilities in Australia still use land application as a form of beneficial reuse for management of biosolids generated from treatment operations. Emerging evidence regarding the risks of various contaminants including endocrine disrupters, antibiotic compounds, per-and polyfluorinated alkyl substances (PFAS) and microplastics has created regulatory uncertainties in Australia around biosolids and waste management. For example, the New South Wales (NSW) Biosolids Guidelines are currently under review by the NSW Environment Protection Authority (EPA). Furthermore, in October 2018, the EPA revoked the general and specific Resource Recovery Orders and Resource Recovery Exemptions for the land application of mixed waste organic output (MWOO) produced from household waste at alternative waste treatment facilities, referencing risks associated with contaminants. This demonstrates that both current and potential alternative biosolids and waste management approaches are subject to uncertainties around regulations.

Gasification of biosolids can provide water utilities with financially and economically attractive opportunities. Benefits of sewage sludge/biosolids gasification at WWTPs will include the following:

In Australia, gasification of biosolids is still an emerging technology. While there are currently no large-scale commercial gasification plants treating biosolids in Australia, Logan City Council partnered with Downer and Pyrocal to develop the Logan City Biosolids Gasification Facility at Loganholme Wastewater Treatment Plant. ARENA, through its Advancing Renewables Program contributed $6 million towards the $17 million project. The trials for biosolids gasification have been completed. The process will use gasification, supplemented by an onsite solar power system to produce heat that will subsequently be used as part of a biosolids drying system. The solid residue or biochar containing carbon, phosphorus and potassium could be used as a soil conditioner. Furthermore, the process will reduce approximately 4800 tonnes of CO2-e annually. Logan City Council is currently exploring other markets for biochar.

Adoption of low emission technologies will help Australia in meeting its international climate change obligations. A Long-term Emissions Reduction Strategy is currently under development by the Commonwealth Government, and at its core is Australia’s Technology Investment Roadmap, which highlights priority low emission technologies.

Production of dispatchable low-carbon electricity through implementation of energy from waste and adoption of carbon capture and storage at conventional power plants are key investment opportunities that reduce GHG emissions from the electricity sector.

Commercialisation of hydrogen, biogas, biomethane and carbon capture and storage in the gas sector can result in significant decarbonisation benefits and new opportunities for the transport sector. Replacement of natural gas with biomethane in LNG and CNG applications offers GHG reduction opportunities.

Other investment opportunities gaining traction in Australia include development of small to large-scale EfW facilities, including thermal EfW plants for treatment and management of residual domestic, commercial, industrial, construction and demolition waste, and biological AD facilities for bioenergy generation using source separated organic waste and/or sewage sludge.

Water utilities can adopt a ‘systems thinking’ approach to develop long-term adaptive strategies that turn their wastewater treatment plants into water resource recovery facilities. At these sites, energy self-sufficiency goals and new revenue streams could be pursued through implementation of onsite bioenergy generation and co-digestion of food waste and sewage sludge.

Overall, the pathways towards decarbonisation, while technically feasible, need to balance the energy ‘trilemma’: energy security, energy affordability and environmental outcomes.

Neville Tawona | Neville Tawona is an Associate Process Engineer at SLR Consulting, a global environmental and advisory firm. With qualifications in chemical engineering and global energy & climate policy, Neville has worked across the public and private sectors with a focus on sustainable solutions for major projects. His interests include developing solutions that utilise established and emerging low-emission technologies as pathways towards decarbonisation. Neville has managed and delivered a variety of projects including designing treatment plants for drinking water, environmental impact assessments for major energy from waste projects, technology due diligence for major investment firms and wastewater growth servicing and investment plans for utilities.

Australian Renewable Energy Agency 2020, Australian first biomethane trial for NSW gas network https://arena.gov.au/news/australian-first-biomethane-trial-for-nsw-gas-network/ (accessed 13/01/2021).

Australian Water Association, 2016, Renewable energy powers Bondi treatment plant https://www.awa.asn.au/AWA_MBRR/Publications/Latest_News/Renewable_energy_powers_Bondi_treatment_plant.aspx (accessed 15/01/2021).

Bauen, A., Berndes, G., Junginger, M., Londo, M., Vuille, F., Ball, R., Bole, T., Chudziak, C., Faaij, A., Mozaffarian, H., 2009. Bioenery – A substantiable and reliable energy source: A review of status and prospects. IEA Bioenergy.

Blue Environment, 2020. National Waste Report 2020. Department of Agriculture, Water, and the Environment; Blue Environment.

Clean Energy Regulator, 2016. About the Emissions Reduction Fund. http://www.cleanenergyregulator.gov.au/ERF/About-the-Emissions-Reduction-Fund (accessed 12/01/2021).

COAG Energy Council, 2019. Australia’s National Hydrogen Strategy. Australian Government Department of Industry, Innovation and Science.

Department of the Environment 2019. National Waste Policy Action Plan 2019. https://www.environment.gov.au/system/files/resources/5b86c9f8-074e-4d66-ab11-08bbc69da240/files/national-waste-policy-action-plan-2019.pdf (accessed 11/01/2021).

Department of Industry, Science, Energy and Resources, 2020. Technology Investment Roadmap Discussion Paper: A framework to accelerate low emissions technologies

https://consult.industry.gov.au/climate-change/technology-investment-roadmap/supporting_documents/technologyinvestmentroadmapdiscussionpaper.pdf (accessed 10/01/2021).

DIF Capital Partners, undated. Avertas Energy- Waste-to-energy project https://www.dif.eu/investments/avertas-energy/ (accessed 15/01/2021).

Energy Networks Australia, 2017. Gas Vision 2050. Reliable, secure energy and cost-effective carbon reduction. Energy Networks Australia.

Energy Networks Australia, 2019. Gas Vision 2050. Hydrogen Innovation Delivering on the Vision. Energy Networks Australia.

Energy Networks Australia, 2020. Gas Vision 2050. Delivering a Clean Energy Future. Energy Networks Australia.

Fagerström, A., Al Seadi, T., Rasi, S., Briseid, T., 2018. The role of Anaerobic Digestion and Biogas in the Circular Economy. IEA.

Freund, P., & Kaarstad, O., 2007: Keeping the lights on. Universitetsforlaget, Oslo.

International Energy Agency, 2019. The Future of Hydrogen: Seizing todays opportunities. IEA. https://www.iea.org/reports/the-future-of-hydrogen (accessed 15/01/2021).

KPMG, 2018. Bioenergy State of the Nation Report: A report on Australia’s bioenergy performance. Bioenergy Australia.

McCabe, B., Kroebel, R., Pezzaglia, M., Lukehurst, C., Lalonde, C., Wellisch, M., Murphy, J.D., 2020. Integration of Anaerobic Digestion into Farming Systems in Australia, Canada, Italy, and the UK. IEA

Tarallo, S., Shaw, A., Kohl, P., Eschborn, R., 2015. A guide to net-zero energy solutions for water resource recovery facilities. Water Environment Research Foundation.

Tarukado, T., Yokoyama, T., Izumiya, T., Maghon, T., 2019. Incineration technologies for various waste conditions. Earth and Environmental Science 265.

United Nations Framework Convention on Climate Change., 2008. Kyoto Protocol reference manual on accounting of emissions and assigned amount. UNFCC.

{kind=link}